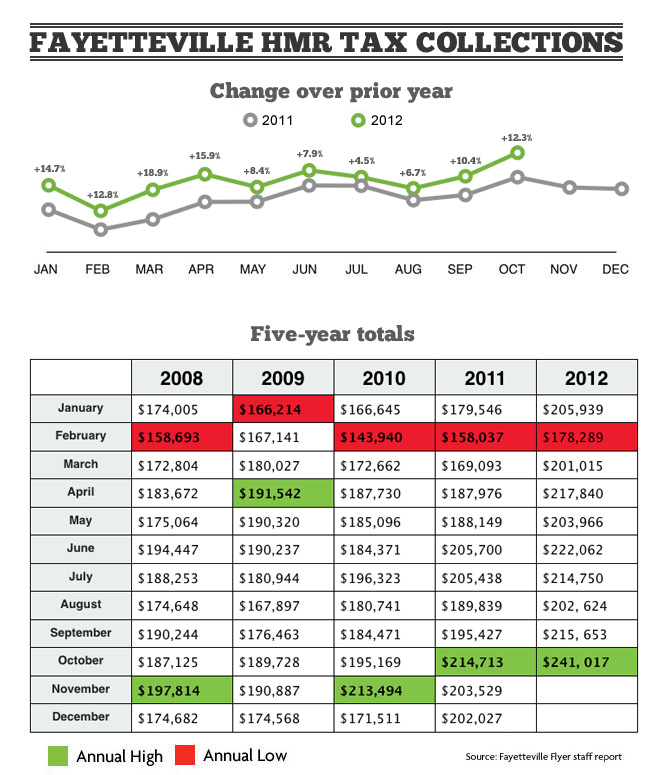

Fayetteville’s hotel, motel and restaurant (HMR) tax receipts saw another record-high month this year compared to the same months in past years.

A&P receipts reported in October were $241,017, a 12.3 percent increase over the same month last year.

Marilyn Heifner, executive director of the A&P Commission, said HMR sales in September were the highest they’ve ever been in Fayetteville. There were three Razorback home football games in September – Jacksonville State, Alabama, and Rutgers – plus the annual Bikes, Blues & BBQ motorcyle rally.

Overall 2012 collections are at $2,103,155 which is an 11 percent increase on the year.

Below is a graph showing 2012 vs. 2011 numbers and a table representing HMR tax collections for the past five years in Fayetteville.

Note: The figures discussed in this post reflect the A&P Commission’s half of the 2 percent tax on hotel and motel stays and food purchases in restaurants. The October report represents September sales.

A&P Funds

Legislation created the Advertising and Promotion Commission in 1977 with the passage of the Hotel, Motel, Restaurant (HMR) tax in Fayetteville. The 2 percent tax is split equally between the city’s Parks and Recreation Department and the A&P Commission. The parks money is used for parks maintenance, operations and for capital improvements. The self-reported numbers do not include retail or liquor sales.

» See recent collection totals

By state legislation, all HMR funds shall be used:

1. for advertising and promoting the city and its environs

2. for the construction, reconstruction, equipment, improvement, maintenance, repair, and operation of a convention center

3. for the operation of tourist promotion facilities in the city

4. for personnel and agencies necessary to conduct the business of the A & P commission

HMR funds can also be used for:

1. for funding the arts

2. for operation of tourist-oriented facilities

3. for construction, reconstruction, repair, maintenance, improvement, equipping and operation of public recreation facilities and for the payment of bonds.

Taxes shall not be used for:

1. general capital improvements within the city

2. costs associated with general operation of the city

3. general subsidy of any civic group or chamber of commerce

Source: Arkansas Code / § 26-75-606 – Use of funds collected